Reasonable Cause For Not Filing Form 2553 Timely - It might also include relying on someone else, such as your accountant, to make the election but that person failed to file form 2553 on time. Tried to prevent a foreseeable failure to file on time Web if you can show reasonable cause for failing to file accurate, timely information returns or payee statements, we may consider penalty relief if you prove: Web the corporation has reasonable cause for its failure to timely file form 2553 and has acted diligently to correct the mistake upon discovery of its failure to timely file form 2553; Web what might those issues be? Web the entity intended to be classified as an s corporation, is an eligible entity, and failed to qualify as an s corporation solely because the election was not timely; Web reasonable cause includes being unaware of when and how to make a late s corporation election. Well, usually one of the following: Requested extensions of time to file when possible; The entity has reasonable cause for its failure to make the election timely;

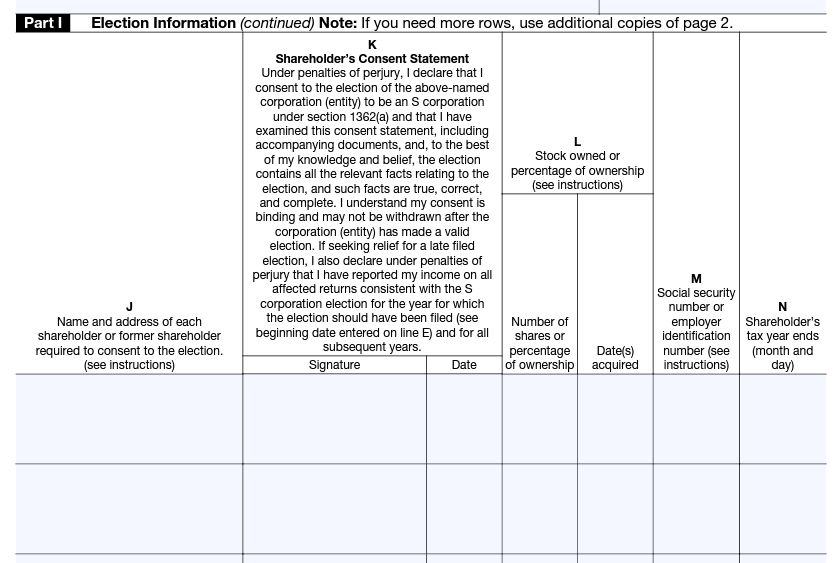

How to Fill in Form 2553 Election by a Small Business Corporation S

Web the entity intended to be classified as an s corporation, is an eligible entity, and failed to qualify as an s corporation solely because the election was not timely; It might also include relying on someone else, such as your accountant, to make the election but that person failed to file form 2553 on time. Web according to the.

Form 2553 pdf Fill out & sign online DocHub

Reasonable cause does not include wanting to reduce your tax liability after the fact. Web reasonable cause includes being unaware of when and how to make a late s corporation election. Requested extensions of time to file when possible; Form 2553 will be filed within 3 years and 75 days of the date entered on line e of form 2553;.

Election of 'S' Corporation Status and Instructions Form 2553

Requested extensions of time to file when possible; You acted in a responsible manner both before and after the failure by having: Web if you can show reasonable cause for failing to file accurate, timely information returns or payee statements, we may consider penalty relief if you prove: Form 2553 will be filed within 3 years and 75 days of.

IRS Form 2553 Who Needs It and How to File It

Web the entity intended to be classified as an s corporation, is an eligible entity, and failed to qualify as an s corporation solely because the election was not timely; Requested extensions of time to file when possible; Failing to make the election in a timely manner. Well, usually one of the following: Web reasonable cause includes being unaware of.

Form 2553 template

Reasonable cause does not include wanting to reduce your tax liability after the fact. Web according to the irs, corporations electing s corporation status must complete and file form 2553, election by a small business corporation no later than two months and 15 days after the start of. It might also include relying on someone else, such as your accountant,.

How To Fill Out Form 2553 for Scorps and LLCs

Tried to prevent a foreseeable failure to file on time Web reasonable cause includes being unaware of when and how to make a late s corporation election. Web according to the irs, corporations electing s corporation status must complete and file form 2553, election by a small business corporation no later than two months and 15 days after the start.

3 Reasons to File a Form 2553 for Your Business

Web reasonable cause includes being unaware of when and how to make a late s corporation election. Web the entity intended to be classified as an s corporation, is an eligible entity, and failed to qualify as an s corporation solely because the election was not timely; Reasonable cause does not include wanting to reduce your tax liability after the.

IRS Form 2553 ≡ Fill Out Printable PDF Forms Online

Web the corporation has reasonable cause for its failure to timely file form 2553 and has acted diligently to correct the mistake upon discovery of its failure to timely file form 2553; Web reasonable cause includes being unaware of when and how to make a late s corporation election. Form 2553 will be filed within 3 years and 75 days.

Learn How to Fill the Form 2553 Election by a Small Business

Well, usually one of the following: Failing to make the election in a timely manner. Tried to prevent a foreseeable failure to file on time Web according to the irs, corporations electing s corporation status must complete and file form 2553, election by a small business corporation no later than two months and 15 days after the start of. Web.

IRS Form 2553 Instructions How and Where to File This Tax Form

Web the corporation has reasonable cause for its failure to timely file form 2553 and has acted diligently to correct the mistake upon discovery of its failure to timely file form 2553; Web the entity intended to be classified as an s corporation, is an eligible entity, and failed to qualify as an s corporation solely because the election was.

Failing to make the election in a timely manner. Web the corporation has reasonable cause for its failure to timely file form 2553 and has acted diligently to correct the mistake upon discovery of its failure to timely file form 2553; It might also include relying on someone else, such as your accountant, to make the election but that person failed to file form 2553 on time. Tried to prevent a foreseeable failure to file on time Web what might those issues be? Reasonable cause does not include wanting to reduce your tax liability after the fact. Web if you can show reasonable cause for failing to file accurate, timely information returns or payee statements, we may consider penalty relief if you prove: Well, usually one of the following: You acted in a responsible manner both before and after the failure by having: The entity has reasonable cause for its failure to make the election timely; Web according to the irs, corporations electing s corporation status must complete and file form 2553, election by a small business corporation no later than two months and 15 days after the start of. Form 2553 will be filed within 3 years and 75 days of the date entered on line e of form 2553; Web the entity intended to be classified as an s corporation, is an eligible entity, and failed to qualify as an s corporation solely because the election was not timely; Web reasonable cause includes being unaware of when and how to make a late s corporation election. Requested extensions of time to file when possible;