What Is Credit Conversion Factor - There has been debate on the suitability of the ccf for ead modelling. Exposure is calculated as the committed but undrawn amount multiplied by a credit conversion factor (ccf). In the advanced approach, ead for undrawn commitments may be calculated as the committed but undrawn amount multiplied by a ccf or derived from direct estimates of total facility ead. This article argues that ccf is unlikely to be appropriate and proposes alternative modeling approaches for exposure at default (ead) in the basel ii accord. Web credit conversion factor (ccf) is the ratio of the estimated additional drawn amount during the period up to 12 months before default over the undrawn amount at the time of estimation. Web the credit conversion factor (ccf), the proportion of the current undrawn amount that will be drawn down at time of default, is used to calculate the ead and poses modelling challenges with its bimodal distribution bounded between zero and one. Web the ccf converts an off balance sheet exposure to its credit exposure (risk weighted assets) equivalent. Web the risk weight that is associated with the exposure prior to the application of the framework does not already factor in any aspect of the credit protection. (2) the entity selling credit protection is a bank 2,. Web in the foundation approach, ead is calculated as the committed but undrawn amount multiplied by a credit conversion factor (ccf).

Credit Conversion Factor Table In Powerpoint And Google Slides Cpb

Web credit conversion factor (ccf) is the ratio of the estimated additional drawn amount during the period up to 12 months before default over the undrawn amount at the time of estimation. Web the credit conversion factor (ccf), the proportion of the current undrawn amount that will be drawn down at time of default, is used to calculate the ead.

Distribution of the Credit Conversion Factor (after truncation

There has been debate on the suitability of the ccf for ead modelling. Web credit conversion factor (ccf) is the ratio of the estimated additional drawn amount during the period up to 12 months before default over the undrawn amount at the time of estimation. Web the risk weight that is associated with the exposure prior to the application of.

PPT Peru Basel II implementation PowerPoint Presentation, free

Web the risk weight that is associated with the exposure prior to the application of the framework does not already factor in any aspect of the credit protection. Web the ccf converts an off balance sheet exposure to its credit exposure (risk weighted assets) equivalent. Web the credit conversion factor (ccf), the proportion of the current undrawn amount that will.

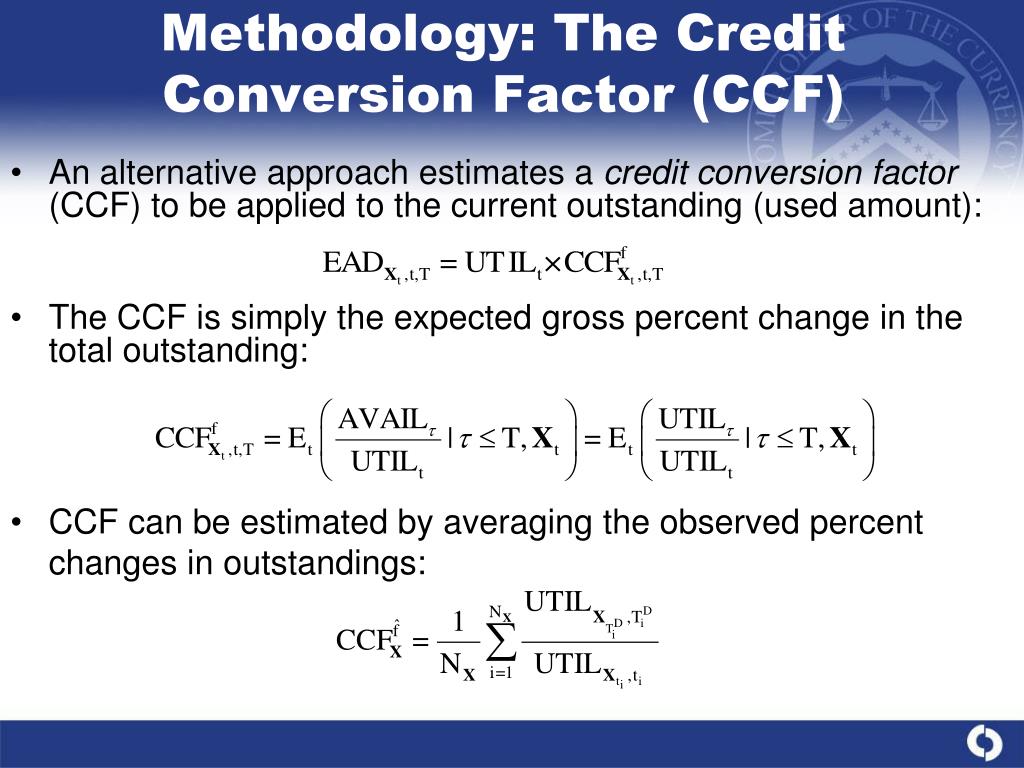

PPT An Empirical Study of Exposure at Default PowerPoint Presentation

Web the ccf converts an off balance sheet exposure to its credit exposure (risk weighted assets) equivalent. Web the risk weight that is associated with the exposure prior to the application of the framework does not already factor in any aspect of the credit protection. Web in the foundation approach, ead is calculated as the committed but undrawn amount multiplied.

An Empirical Study of Exposure at Default

This article argues that ccf is unlikely to be appropriate and proposes alternative modeling approaches for exposure at default (ead) in the basel ii accord. Web the risk weight that is associated with the exposure prior to the application of the framework does not already factor in any aspect of the credit protection. (2) the entity selling credit protection is.

Credit Conversion Factors for Off Balance Sheet Items Download Table

There has been debate on the suitability of the ccf for ead modelling. (2) the entity selling credit protection is a bank 2,. Web the credit conversion factor (ccf), the proportion of the current undrawn amount that will be drawn down at time of default, is used to calculate the ead and poses modelling challenges with its bimodal distribution bounded.

Capital Adequacy Norms Credit Conversion Factor for Off Balance Sheet

There has been debate on the suitability of the ccf for ead modelling. (2) the entity selling credit protection is a bank 2,. Web the risk weight that is associated with the exposure prior to the application of the framework does not already factor in any aspect of the credit protection. Web in the foundation approach, ead is calculated as.

Capital adequacy Basel 2. Financial institutions management kimep

Web the ccf converts an off balance sheet exposure to its credit exposure (risk weighted assets) equivalent. Web the credit conversion factor (ccf), the proportion of the current undrawn amount that will be drawn down at time of default, is used to calculate the ead and poses modelling challenges with its bimodal distribution bounded between zero and one. In the.

(PDF) Exposure At Default Models with and without the Credit Conversion

Web the risk weight that is associated with the exposure prior to the application of the framework does not already factor in any aspect of the credit protection. Web credit conversion factor (ccf) is the ratio of the estimated additional drawn amount during the period up to 12 months before default over the undrawn amount at the time of estimation..

PPT Capital Adequacy PowerPoint Presentation ID147923

Web credit conversion factor (ccf) is the ratio of the estimated additional drawn amount during the period up to 12 months before default over the undrawn amount at the time of estimation. (2) the entity selling credit protection is a bank 2,. This article argues that ccf is unlikely to be appropriate and proposes alternative modeling approaches for exposure at.

Web the risk weight that is associated with the exposure prior to the application of the framework does not already factor in any aspect of the credit protection. Web credit conversion factor (ccf) is the ratio of the estimated additional drawn amount during the period up to 12 months before default over the undrawn amount at the time of estimation. Web the ccf converts an off balance sheet exposure to its credit exposure (risk weighted assets) equivalent. Web in the foundation approach, ead is calculated as the committed but undrawn amount multiplied by a credit conversion factor (ccf). In the advanced approach, ead for undrawn commitments may be calculated as the committed but undrawn amount multiplied by a ccf or derived from direct estimates of total facility ead. This article argues that ccf is unlikely to be appropriate and proposes alternative modeling approaches for exposure at default (ead) in the basel ii accord. There has been debate on the suitability of the ccf for ead modelling. Exposure is calculated as the committed but undrawn amount multiplied by a credit conversion factor (ccf). Web the credit conversion factor (ccf), the proportion of the current undrawn amount that will be drawn down at time of default, is used to calculate the ead and poses modelling challenges with its bimodal distribution bounded between zero and one. (2) the entity selling credit protection is a bank 2,.